Tag: finance

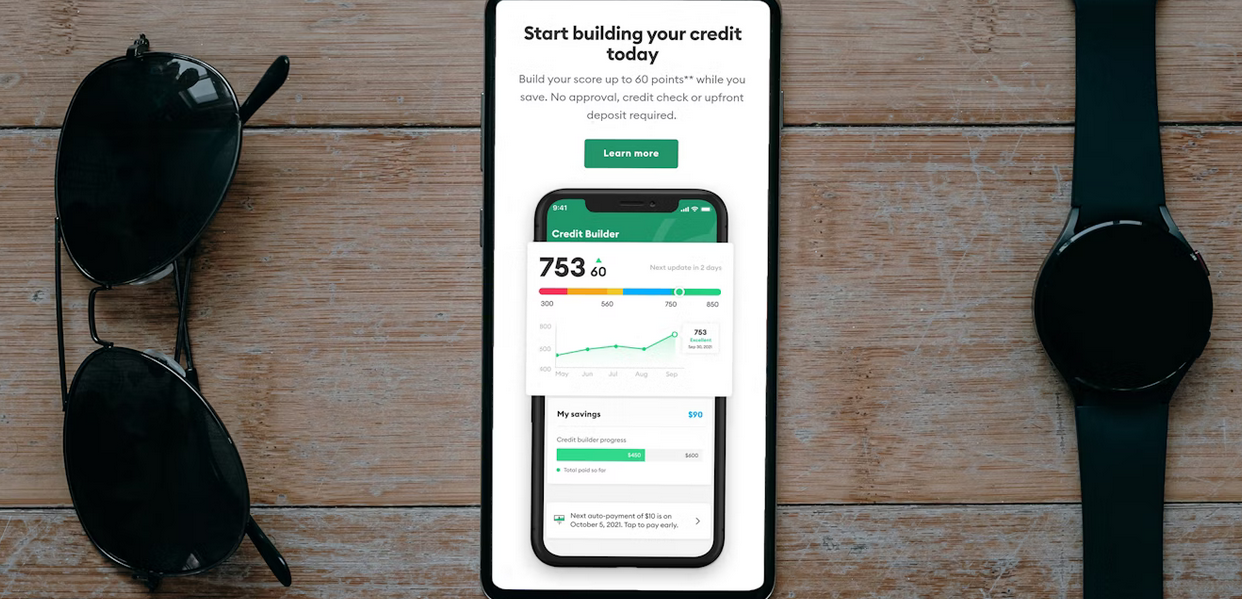

How to Improve Your Credit Score Using Credit Cards

- by Emilie Albury

- 6 months ago

- 0 comments

Improving your credit score might seem like a challenge, but credit cards can actually be one of the simplest tools to help you do just that—if used responsibly. Rather than fearing them, learning how to manage your cards wisely can gradually boost your score and unlock better financial opportunities. Many people misunderstand how credit cards affect their credit standing, leading to habits that do more harm than good. In this guide, we’ll outline five practical and effective strategies you can apply today using your credit card. These methods are not complicated, but they require consistency and self-control. By building better habits around your card usage, you’re not just maintaining your credit—you’re actively improving it over time.

Always Pay on Time—No Exceptions

One of the most important things you can do to improve your credit score using a credit card is to make every payment by the due date. Payment history has a significant portion of your credit score, and one missed payment can set you back for months. Late payments can stays on your credit report for years. Setting automatic payments to cover at least the minimum amount due can prevent accidental delays. Additionally, many credit card apps now allow you to set payment reminders or notifications to help stay ahead. While it’s ideal to pay off your full balance, even minimum payments made on time count in your favor.

Keep Your Credit Utilization Low

Credit utilization is a portion of the credit limit you’re using. If your card has a limit of $1,000 and you routinely carry a $900 balance, this can signal risk to lenders—even if you pay it off. A smart rule is to stay below 30% of your credit limit. In fact, the lower your utilization, the better your score tends to respond. So if you don’t need to carry a high balance, don’t. Consider paying your bill multiple times a month or making an extra payment before the statement date to reflect a lower usage.

Don’t Close Old Accounts Too Soon

While it might seem tempting to close out unused or old credit cards, doing so can hurt your credit score by lowering your total available credit and shortening your credit history. The length of your credit history matters—a longer credit timeline reflects positively on your score. Even if you’re no longer using an old card frequently, keeping it open with the occasional small purchase (paid off quickly) can help support your credit profile. Just be cautious of annual fees; if your old card has one and offers no benefits, consider calling the issuer to downgrade it to a no-fee version instead of closing it outright.

Diversify the Types of Credit You Use

Although credit cards are a great start, using a mix of credit types—such as installment loans or retail accounts—can further strengthen your credit score. This doesn’t mean rushing out to take on debt. But if you’re planning to make a large purchase, such as financing a computer or appliance, consider using a structured loan if it fits your budget. Having both revolving (like credit cards) and installment credit demonstrates that you can handle different kinds of financial obligations, which can gradually nudge your credit score upward.

Review Your Credit Report Regularly

Many consumers never check their credit reports, which is a mistake. Errors can appear that unfairly lower your score, and unless you spot them, they’ll stay there. Obtain a free annual credit report from official sources and review it for accuracy—check your personal details, account information, and payment records. If something doesn’t look right, dispute it promptly. Fixing errors can lead to a quick bump in your credit score. Also, reviewing your report gives you an idea of how your current habits are reflected in your credit profile—helping you course-correct if needed.

Credit cards are effective at building and improving your credit score—but they demand thoughtful handling. By focusing on timely payments, keeping balances low, preserving older accounts, maintaining credit variety, and checking your reports for mistakes, you can create a healthier credit profile over time. These strategies aren’t about tricks or shortcuts—they’re grounded in smart financial behavior that lenders reward. Whether you’re just starting your credit journey or looking to recover from past missteps, your credit card can help steer you in the right direction—one payment at a time.…

Read More

Can Quick Loans Improve Your Credit Score? Here’s the Truth

- by Victor Richmond

- 2 years ago

- 0 comments

If your credit score is going crazy and getting lower and lower, it’s time to make a smart financial move. Improving your credit score actually has lots of paths you can choose from. One popular choice is getting quick loans. You might wonder, can these fast solutions really give your credit a boost? The answer isn’t as simple as yes or no.

Getting a pikalaina heti tilille can have both positive and negative effects on your credit health. In this blog post, we’ll explore how on-time payments can help raise your score, the benefits of diversifying your credit mix, and the consequences of missing payments. Plus, we’ll discuss whether using a quick loan to pay off existing debt could be a smart move for you. Let’s dive straight into the details.

On-Time Payments Boost Your Score

One of the simplest ways to enhance your credit score is through on-time payments. Every month, when you make timely payments on a quick loan, you’re ultimately sending a positive signal to credit bureaus. These punctual payments show that you’re responsible and reliable with borrowed money.

Over time, this consistency builds trust in your financial habits. Even a single late payment can have lasting consequences. A missed deadline might drop your score significantly and undo months of effort. It’s crucial to stay organized and set reminders if needed. By prioritizing these payments, you not only maintain good standing but also pave the way for future loans or credit opportunities.

Diversifying Your Credit Mix Can Benefit Your Credit Score

A healthy credit score often hinges on your credit mix. This refers to the unique variety of credit accounts you hold, such as revolving accounts like credit cards and installment loans like personal or quick loans. When lenders see a diverse portfolio, they’re more likely to view you as a responsible borrower. It signals that you can manage different types of debt effectively. That said, adding a quick loan to your mix might eventually help improve your overall score if managed well. This shows creditors you’re capable of handling various financial responsibilities.

Missing Payments on a Quick Loan Can Harm Your Credit Score

Without a doubt, when you take out a loan, lenders expect timely repayments. Failing to meet these obligations signals financial instability. Each missed payment gets reported to credit bureaus. This negatively impacts your credit report and can lower your score significantly. A single late payment might seem minor but its effects linger for years.

Moreover, the longer you wait to make that payment, the worse it gets. Late fees accumulate, and the lender may escalate their collection efforts. This not only adds stress but could further damage your financial reputation. In short, missing payments is a slippery slope that affects more than just one aspect of your finances; it influences future borrowing opportunities as well.

Using the Loan to Pay Off Credit Card Debt Can Lead to a Higher Credit Score

Using a quick loan to pay off credit card debt can also be a strategic move for your financial health. Credit cards often carry high interest rates, and consolidating that debt into a single loan may reduce the overall interest you pay. When you pay off those balances, your credit utilization ratio decreases. Lenders typically prefer borrowers who use less of their available credit. A lower ratio signals responsible usage, which can give your score a boost. Moreover, having fewer open accounts means managing payments becomes simpler. This streamlined approach makes it easier to stay on top of deadlines and maintain an on-time payment history—another critical factor in improving your score.

So, should you get a quick loan? Before answering to this question, you need to weigh the pros and cons carefully. Whether or not you should get a quick loan depends on your individual financial situation and goals. Just be sure you’re informed and ready for the commitment involved with taking out such a loan—your credit future might depend on it.…

Read More

Understanding Tax Debt Resolution: The Role of IRS Tax Relief Programs

- by Emilie Albury

- 2 years ago

- 0 comments

Tax debt can be a daunting burden for individuals and businesses alike, leading to financial stress and uncertainty. However, the Internal Revenue Service offers an IRS forgiveness program designed to help taxpayers resolve their tax debt and regain financial stability. In this article, we will explore these IRS tax relief programs and their vital role in assisting taxpayers in times of financial hardship.

Offer in Compromise (OIC)

The Offer in Compromise program is one of the most well-known IRS tax relief programs. It allows eligible taxpayers to settle their tax debt for less than the full amount owed. To qualify, you must demonstrate that paying the full amount would cause financial hardship or be unjust. The IRS considers factors such as your income, expenses, assets, and ability to pay.

Installment Agreements

Installment agreements provide taxpayers with a structured plan to pay off their tax debt over time. These agreements allow you to make regular monthly payments, making it easier to manage your financial obligations. The IRS offers various types of installment agreements, depending on the amount you owe and your financial situation.

Innocent Spouse Relief

Innocent Spouse Relief is designed to protect individuals who may be held responsible for their spouse’s tax debt. If you can prove that you had no knowledge of your spouse’s tax errors or omissions, you may qualify for relief. This program helps innocent spouses avoid unfair tax liability.

Currently Not Collectible (CNC) Status

If you are facing financial hardship and cannot afford to pay your tax debt, you may be eligible for Currently Not Collectible status. This temporarily suspends IRS collection efforts until your financial situation improves. While in CNC status, the IRS will not attempt to collect the debt but may still accrue penalties and interest.

Tax Liens and Levies Resolution

IRS tax relief programs also address tax liens and levies. A tax lien is a legal claim against your property, while a levy allows the IRS to seize your assets to satisfy a tax debt. The IRS offers options to release or remove tax liens and stop levies, such as entering into an installment agreement or demonstrating financial hardship.

Fresh Start Initiative

The Fresh Start Initiative is a collection of IRS tax relief provisions designed to make it easier for individuals and businesses to resolve their tax debt. It includes more flexible criteria for Offer in Compromise, streamlined installment agreements, and increased thresholds for tax liens.

Tax Relief for Disaster Victims

In times of natural disasters, the IRS provides special tax relief programs for affected individuals and businesses. This relief may include extended filing deadlines, penalty waivers, and assistance in reconstructing lost tax records.

IRS tax relief programs play a crucial role in helping taxpayers resolve their tax debt and regain financial stability. Whether you are struggling with a substantial tax debt or facing unexpected financial challenges, it’s essential to explore the options available to you. Consulting with a tax professional or seeking assistance from the IRS can help you determine the best course of action for your specific situation. Remember that proactive communication with the IRS is often the first step toward finding a suitable tax debt resolution plan.…

Read More

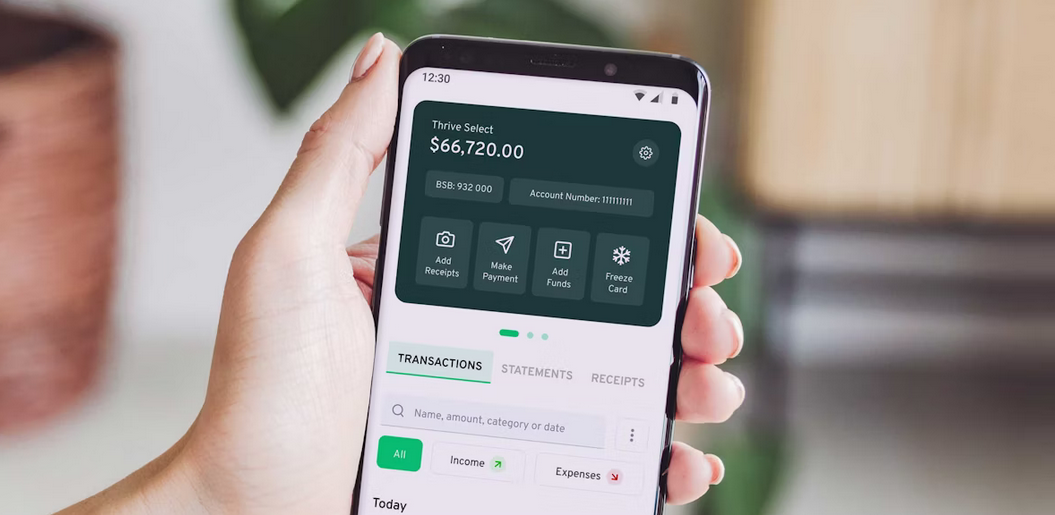

Simple Hacks to Take Your Credit Card Rewards to the Next Level

- by Benjamin Garza

- 3 years ago

- 0 comments

Juggling with kids while working at home and managing the finances – all at the same time is a challenge for anyone. But hey, busy moms! Did you know that those credit card(s) that are tucked away in your wallet can help you get rewards and more? Yes, that’s right. With the bästa kreditkortet or credit card reward programs, you can get money back on all of your purchases, as well as special discounts and deals.

The banks and issuers of these cards provide cash rewards, airline miles, points for shopping, gift certificates, and more for using the card. Now let me ask you a question. Are you ready to max out the rewards and get the most bang for your buck? So read on for some simple hacks that can help you do just that.

Consider Going for a “Product Change”

First off, let’s evaluate how much you are getting from your current credit card. Is it enough? If not, why not consider doing a “product change” – changing the type of credit card you currently have? Many banks and issuers run special campaigns offering higher reward points on various types of cards like travel, gas, dining, and so on. Do your research and find out which card will provide you with the best rewards. Without applying for a new card, you can get more rewards by doing a product change.

Ask for a Retention Offer

Have you noticed that some of your cards have been sitting idle in your wallet? It may be time to call the issuer and ask for a retention offer. Many banks will give bonus points, rewards, or discounts if you start using their card again. This will be such a great opportunity to get the most out of your card and enhance your rewards. Just be sure to read the fine print and ask questions if needed.

Be Aware of the Credit Card Calendar

The credit card market is constantly evolving. They have great offers and rewards points that can be availed during different times of the year. For example, banks usually come out with special campaigns around holidays such as Christmas and Thanksgiving. Doing your due diligence to keep up with the ever-changing promotions will help you get more rewards points and discounts on all your purchases.

Pay Attention to the Bank’s Promotions

Banks and credit card issuers often come up with new promotions that can help you maximize your rewards points. They may offer discounts on certain products or services, bonus points for a specific purchase amount, cash back offers, and so on. So make sure to read their emails, flyers, and other materials to know what they are offering, and take advantage of the same. In some cases, you may even be eligible for additional rewards and discounts – so don’t miss out on those opportunities.

Finally, make sure you use your credit card responsibly. Pay off your balance in full each month to avoid carrying debt or paying interest. This way, you’ll be able to maximize your reward points and get more out of them. With these simple hacks, you can take your credit card rewards to the next level and get the most bang for your buck. So moms, get outside your comfy zone and make the most of your card.…

Read More

What to Consider When Choosing a Credit Repair Company in Las Vegas

- by Victor Richmond

- 4 years ago

- 0 comments

Choosing a credit repair company in Las Vegas is not as easy as it might seem. There are many options to choose from, and they vary significantly in terms of services they offer and the types of results they can produce. This blog post will discuss some of the most important things you should consider when choosing credit repair.

Consider Size of the Company

Large and well-known companies often have more experience than smaller companies. At the same time, they might not be as interested in working with you precisely because their reputation is already solidified within the industry. On the other hand, a small company will likely have fewer resources to offer but could provide extra services at no additional charge or only a minimum fee because they are so well known.

Large and well-known companies often have more experience than smaller companies. At the same time, they might not be as interested in working with you precisely because their reputation is already solidified within the industry. On the other hand, a small company will likely have fewer resources to offer but could provide extra services at no additional charge or only a minimum fee because they are so well known.

It can be challenging to determine how long it will take for your credit report to improve, but most companies can provide some estimate of the time you will need. Having good credit can help you qualify for mortgages, lower interest rates on car loans, and even give you access to better offers with certain retailers in some cases.

Ask For References From Past Clients

A company that can provide references from past customers can demonstrate their experience and expertise in the industry. This will allow you to understand better what services they offer, how well they perform them, and whether or not it’s something you would be interested in doing for yourself.

Credit repair is a tricky business, and not all companies can provide the same level of results. Checking into a company’s track record will help you determine how successful they have been in the past and whether or not their methods are likely to work for your specific credit situation.

Check Their Fee Structure and What Services They Offer

There are quite a few different companies that offer credit repair services, and each one charges their fee for the specific services they provide. If you think your situation might require additional help, such as debt settlement or bankruptcy advice, make sure to ask about this before signing any paperwork because it will mean additional fees on top of what you already paid.

There are quite a few different companies that offer credit repair services, and each one charges their fee for the specific services they provide. If you think your situation might require additional help, such as debt settlement or bankruptcy advice, make sure to ask about this before signing any paperwork because it will mean additional fees on top of what you already paid.

At the same time, it can be helpful to know what services they offer so that you can determine whether or not their plan of action is something you would like them to do for your specific situation.…

Read More

Why Personal Financial Planning is Important

- by Emilie Albury

- 5 years ago

- 0 comments

If you are not prepared, there are a ton of surprises involving finances you can encounter, which eventually can overwhelm you. It can be school fees, medical bills, or even car issues. That is why personal financial planning is vital as it helps you plan both your current and future lifestyle.

You can either develop your financial plan or seek professional financial services from qualified financial advisors. A detailed financial plan guides you on various financial investments like budgeting, insurance, investing, savings, and any other thing that involves finances.

Here is why personal financial planning is crucial.

Budgeting Your Money

As stated above, you can get a lot of financial surprises if you are not adequately prepared. You need to effectively budget your income to cover your monthly expenses and remain with a reserve that will cover any future or unexpected financial emergencies. That is where personal financial planning comes in.

As stated above, you can get a lot of financial surprises if you are not adequately prepared. You need to effectively budget your income to cover your monthly expenses and remain with a reserve that will cover any future or unexpected financial emergencies. That is where personal financial planning comes in.

It helps you create a spending plan for each month, but you should also make sure you implement the budget. Having a budget with a professional’s touch from a qualified financial planner allows you to make well-informed personal financial decisions. It gives you a clear insight into the things you should spend on and the things to avoid.

Help to Measure Your Progress on Financial Goals

The main essence of coming up with a personal financial plan is because you have financial goals you intend to meet. You cannot set these goals without creating a financial plan first. However, you should ensure that your goals are achievable to avoid straining yourself to the extremes. You can set aside a specific amount of money monthly to contribute to a savings plan or repaying a loan. You can quickly achieve your targets with a financial plan in place as it gets you to be more disciplined financially.

Expense Cutting

One of the primary reasons why people often have financial troubles is because of impulsive buying. You see an item you like, buy it immediately and forget that you had a debt to settle or a savings plan to adhere to. Creating a personalized financial plan helps you develop a budget that, if adhered to, helps cut down on unnecessary expenses. The plan gives details on how you can spend your money and how you can also save for your future.

You get to identify the essential expenses but also but a small budget aside for entertainment purposes. The remainder can be set aside as saving for future financial needs or any financial emergencies.…

Read More

Benefits of Financial Technology

- by Benjamin Garza

- 9 years ago

- 0 comments

Financial technology is widely known as FinTech, and it is the use of technology to deliver financial products and services. There is a wide range of financial products and services that can be provided by innovative technology. Such products and services include convenient and fast methods of payments by the consumer. In other words, improving the clients’ user experience. Many business segments have benefited from this innovation. For instance, mobile payments, lending, and money transfer among other transactions. Many consumers have greatly benefited from the rapid growth of the innovation, and this has ultimately helped businesses because they have reduced costs. In addition to this, there is a healthy competitive environment between the companies. Here are some benefits of financial technology.

Better Payment Systems

This technology has enabled businesses to be more effective than they were before because the invoices are accurate and the method of collection of payment is effective. In addition to this, consumers are often attracted to convenience. Therefore, for those businesses that have adopted this technology, there is a chance that they have retained their customers and increased their customer base because of their convenient, professional services.

This technology has enabled businesses to be more effective than they were before because the invoices are accurate and the method of collection of payment is effective. In addition to this, consumers are often attracted to convenience. Therefore, for those businesses that have adopted this technology, there is a chance that they have retained their customers and increased their customer base because of their convenient, professional services.

Rate of Approval

Reports show that many small vendors are starting to use lenders who are involved in financial technology. This is because such lenders are most likely to increase the accessibility and hasten the rate of approval for finance. A while ago, the application process was time-consuming. However, with financial technology, the application process and receiving of the capital is a process that takes just about 24 hours.

Advanced Security

For people to confident in the financial services, they are using, applying the latest security techniques is needed. Many mobile technologies are being invented that are highly effective in ensuring that consumers have maximum data privacy and that the data is secure. Some of the latest security options include the biometric data and encryption.

For people to confident in the financial services, they are using, applying the latest security techniques is needed. Many mobile technologies are being invented that are highly effective in ensuring that consumers have maximum data privacy and that the data is secure. Some of the latest security options include the biometric data and encryption.

Convenience

The companies that are involved with financial technology often use mobile connectivity. This has therefore increased the number of customers who can have access to these kinds of services. In addition to this, the efficiency and convenience of transactions are significantly improved. Consumers now have the option to manage their finances using their smart-phones and tablets, and this has enabled the business to provide their consumers with an all-round experience thus improving the consumer experience.…

Read More